Any deviation from the general tax regime laid down in the state laws which provides for a reduction in the tax burden or more favourable tax payment procedures for a taxpayer or a group of taxpayers may be regarded as a tax relief on the basis of the criterion that the taxpayer or a group thereof conforms to a characteristic specified in the tax law (amount of income, marital status, type of economic activity, region, etc.).

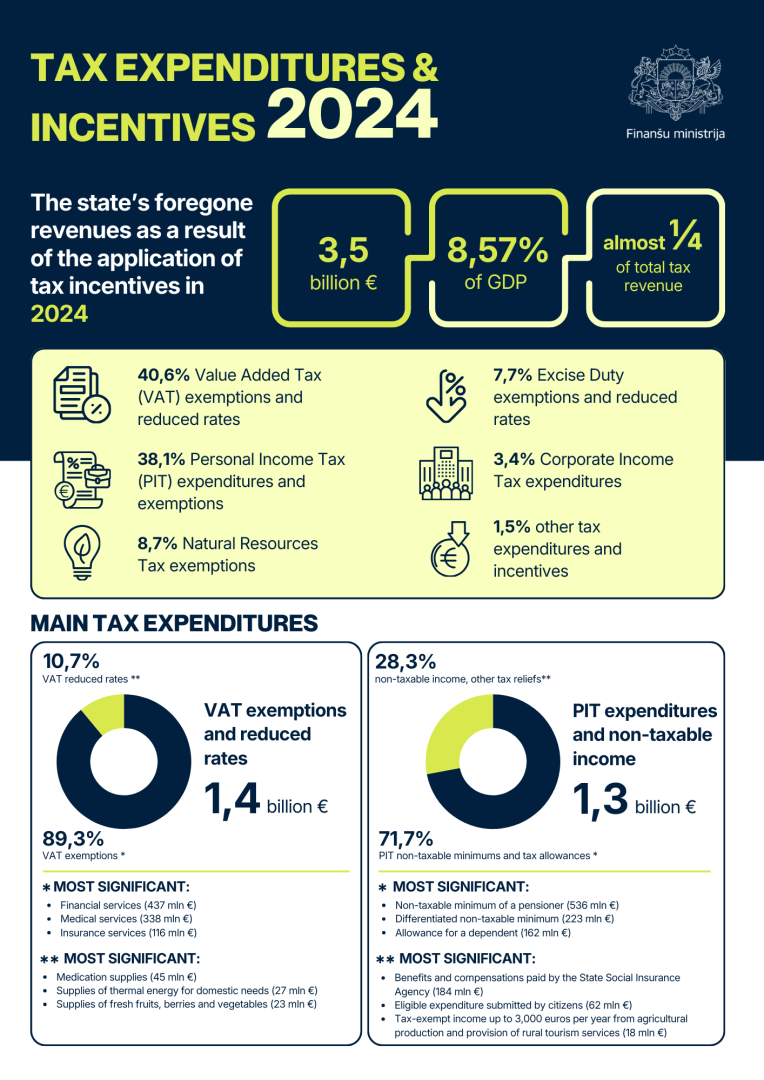

There are currently more than 300 different tax incentives in Latvia. According to the calculations of the Ministry of Finance tax expenditures in 2024 were around 3.5 billion euro, which is 8.57% of GDP and amounting for almost ¼ of the total tax revenue. The tax expenditures in 2024 compared to 2023, increased by 251.5 million euro, or by 7.8%. In 2024, there has been a significant increase in the tax expenditures from the application of value added tax relief (by 100.7 million euro, or by 7.7%) and from the application of excise tax relief (by 59.4 million euro, or by 28.7%).